business loans michigan, small business loans michigan, personal loans in michigan

Understanding Different Types of Business Loans

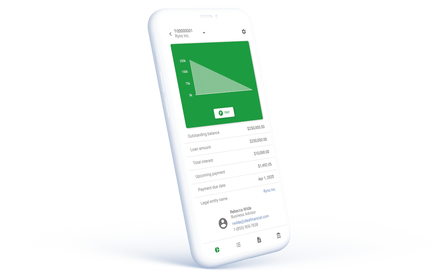

When exploring financing options, it's essential to understand the various types of business loans available. Each type serves different purposes and can cater to specific business needs. Common categories include term loans, lines of credit, and SBA loans, each with unique features and benefits that can help businesses grow.

For instance, term loans provide a lump sum of cash for significant investments and are repaid over a set period, while lines of credit offer flexible access to funds as needed. Understanding these distinctions allows business owners to choose the most suitable financing option for their operational requirements and growth objectives.

The Application Process for Business Loans

The application process for obtaining a business loan can seem daunting, but understanding the steps involved can simplify it significantly. Typically, the process begins with gathering necessary documentation, such as financial statements, tax returns, and a solid business plan to present to lenders.

Once the documentation is prepared, business owners can submit their applications, which may include an online form or a direct meeting with a loan officer. The lender will then review the application, assess creditworthiness, and determine loan eligibility, which can lead to approval in as little as 24 hours for some loans.

Tips for Choosing the Right Business Financing

Selecting the right financing option is crucial for the success of any business venture. Business owners should consider factors such as interest rates, repayment terms, and the specific purpose of the loan when making their decision. Additionally, understanding the total cost of the loan, including any fees or hidden charges, is vital.

Engaging with a financial advisor can also provide valuable insights, helping entrepreneurs navigate the complexities of business loans and find the best solution tailored to their unique circumstances. This strategic approach can lead to more informed decisions and better financial outcomes.

Common Mistakes to Avoid When Applying for Business Loans

Many business owners make critical mistakes during the loan application process that can hinder their chances of approval. One common error is failing to prepare financial documentation thoroughly, which can raise red flags for lenders and delay the process.

Another mistake is applying for loans without a clear understanding of the terms and conditions. Business owners should avoid rushing through the application and take the time to research and compare different lenders to secure the best deal possible. Learning from these pitfalls can enhance the likelihood of obtaining the necessary funding successfully.